The Titans of Global Trade: Unveiling the Giants Behind the Supply Chain

How Major Multinationals Dominate Shipping, Commodities, and Freight Networks in the Modern Economy

Global physical trade – encompassing container shipping, port operations, and commodity logistics – is dominated by a handful of very large multinational firms. These companies control vast fleets of ships, terminals, pipelines, and storage facilities, giving them outsized influence over trade flows and pricing. This report examines the principal players by sector, outlining each firm’s core business, scale, geographic reach, vertical integration, financials (where available), and role in geopolitics or regulation. Where possible, we cite recent data and analyses to quantify market share and performance.

Container Shipping Lines

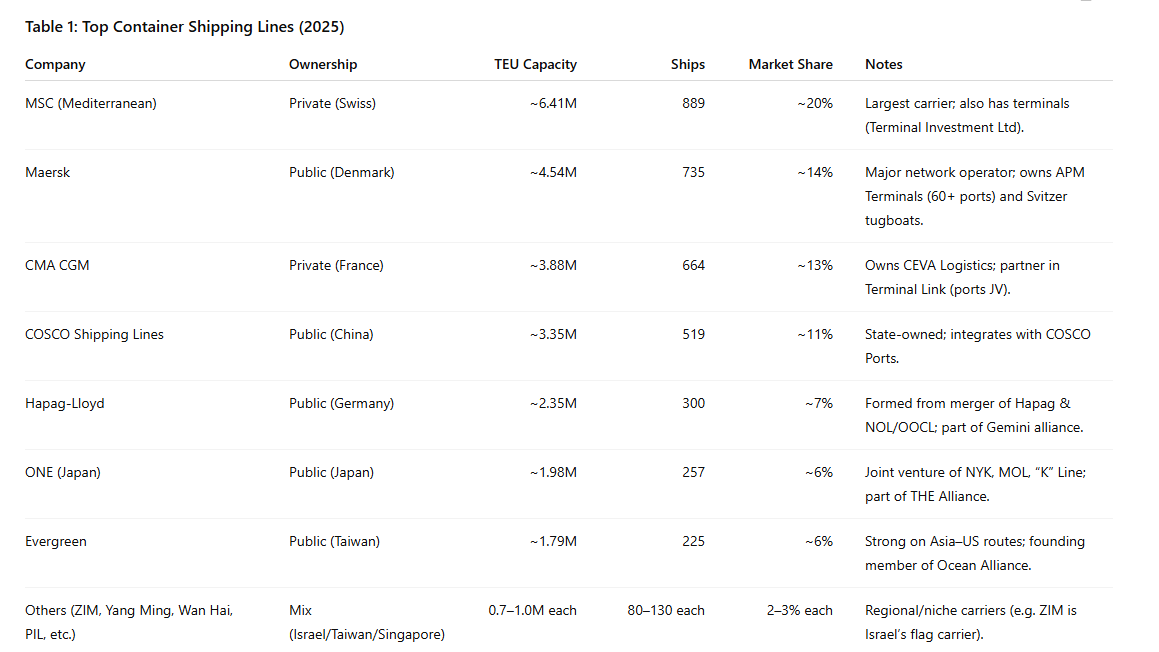

Container shipping is highly concentrated. The top carriers – mostly private or state-affiliated – command the majority of global capacity, measured in TEU (twenty-foot equivalent units). According to Alphaliner, the five largest lines together control over 70% of global container capacity. For example, Mediterranean Shipping Company (MSC) (private, Switzerland) operates ~889 ships totaling ~6.41 million TEU (~20.2% global share), making it the world’s largest carrier. Maersk (public, Denmark) is second with ~735 ships and ~4.54 million TEU (14.3%). Other major carriers include CMA CGM (private, France, 664 ships, ~3.88M TEU, 12.7%), COSCO Shipping Lines (state-owned/Shanghai, 519 ships, ~3.35M TEU, 10.6%), Hapag-Lloyd (public, Germany, 300 ships, 2.35M TEU, 7.4%) and Ocean Network Express (ONE) (joint venture of Japan’s three largest lines, 257 ships, 1.98M TEU, 6.2%). (See Table 1.) Other notable carriers include Evergreen, HMM (Hyundai Merchant Marine), ZIM (Israel), Yang Ming, and Wan Hai (Taiwanese firms). Many of these lines collaborate in large alliances (2M, Ocean Alliance, THE Alliance) to jointly operate routes and share vessels, reflecting an oligopolistic market structure. In recent years, however, some alliances have unraveled (e.g. MSC and Maersk leaving 2M in 2025) as carriers pursue independent networks, indicating dynamic competition despite consolidation.

Vertical integration: Most top carriers have invested vertically. For example, Maersk owns APM Terminals (global port terminals in 60+ locations), and also operates towing, logistics, and digital services. MSC’s parent group (Aponte family) controls MSC Cruises and a growing terminal network (Terminal Investment Ltd, Africa Global Logistics). CMA CGM owns logistics firm CEVA and shares in Terminal Link (ports JV with China Merchants). COSCO’s parent conglomerate encompasses COSCO Shipping Ports, shipyards, and logistics arms. Hapag-Lloyd has less vertical diversification but has acquired regional carriers (PIL) to boost scale. Collectively, these giants coordinate networks: for instance, Maersk and Hapag’s “Gemini” cooperation routes their ships and terminals to gain efficiency.

Market power: The top four carriers (MSC, Maersk, CMA CGM, COSCO) accounted for roughly 57% of capacity by 2025. Such concentration gives them pricing power on key trade lanes. During the COVID-19 disruptions and subsequent freight boom (2020–21), these carriers achieved record profits and rigidly controlled vessel capacity to keep rates high. Even as freight rates have since normalized, the largest lines still reap economies of scale and maintain disciplined capacity growth. (For example, MSC reported it will “go solo” on major East–West trades as its own network priorities.)

Geography: These carriers operate on all global trade routes, but each has regional strengths. Chinese COSCO (and its affiliate OOCL) dominates Asia–Europe and Asia–America services; CMA CGM and MSC cover transatlantic and Asia–Europe lanes; ONE focuses on Asia–Europe and intra-Asia trade; Evergreen is strong on Asia–North America; Hapag-Lloyd is major in Asia–Europe and Latin America; HMM mainly on Asia–Europe/India (as a 2M member); and smaller carriers serve niche markets. All operate global schedules linking major hubs (Shanghai, Singapore, Rotterdam, Los Angeles, etc.).

Financial performance: Shipping lines are typically cyclical. In 2021–22, top carriers saw historically high revenues (Maersk’s revenues peaked at $81B in 2022) and profits; but by 2023–25 margins shrank as rates fell. For example, Maersk’s net profit fell 78% in 2023 as freight rates normalized (though still profitable). Many carriers reported net losses in early 2025 due to overcapacity and competition. Nonetheless, carriers have strong balance sheets (e.g. Maersk had $6.5B net income in 2022, with robust liquidity) and are investing in new ultra-large ships. Public carriers like Maersk, Hapag-Lloyd, and ONE disclose detailed financials, but private ones (MSC, CMA CGM) do not publish full results.

Trends: Digitalization (e.g. Maersk’s blockchain “TradeLens” platform) and automation (e.g. autonomous ships trials) are ongoing industry trends. A major trend is decarbonization: under IMO rules, ships must cut carbon intensity ~30% by 2035 and ~65% by 2040, pushing carriers to adopt LNG, methanol, wind-assist, biofuels, and new designs. For example, Maersk has started commissioning methanol dual-fuel containerships. Alliances may further shift as carriers prioritize in-house networks. Geopolitical factors (e.g. U.S.–China trade tensions, war in Ukraine redirecting cargos, Houthi attacks closing Red Sea routes) can sharply affect capacity deployment and insurance costs.

Table 1: Top Container Shipping Lines (2025)

Global Port Operators

Major shipping lines rely on a network of ports and terminals, many of which are managed by large port-operating firms. The largest by container throughput is PSA International (Singapore), a Temasek-owned authority, which handled a record ~94.8 million TEU in 2023 (~38.8M in Singapore’s Port of Singapore; 56M in global terminals). PSA is expanding its Tuas mega-port to 65M TEU capacity by 2040. Next are Chinese giants: China Merchants Port Holdings (HK-listed subsidiary of state-owned China Merchants Group) and COSCO Shipping Ports (HK-listed, part of COSCO Shipping Corp). In 2023 China Merchants overtook Cosco Ports as China’s largest terminal investor; it now holds stakes in major ports like Ningbo-Zhoushan and is expanding abroad (Indonesia, Brazil) under Beijing’s Belt & Road Initiative. Other top operators include APM Terminals (part of Maersk; ~60 facilities worldwide), DP World (Dubai-based; government-owned but publicly traded, operates ~80 ports), and Hutchison Ports (HK-based, CK Hutchison; ~50 ports globally). DP World is diversifying into logistics, while Hutchison remains a dominant container terminal operator from Asia to Europe. Mid-sized operators include ICTSI (Philippines; 30+ terminals), CMA Terminals (joint venture of China Merchants and CMA CGM), and Yilport (Turkey’s Yildirim Group, minority owner of CMA CGM, expanding globally).

Port operators often have equity stakes in terminals rather than full ownership; Drewry data indicates PSA’s equity share throughput was ~60m TEU in 2023, followed by China Merchants and Cosco Ports (each ~40–50m TEU) and DP World (~30m). (See Table 2.) Many of these firms’ ports sit on strategic chokepoints (e.g. PSA in Singapore, DP World in Jebel Ali and London Gateway, Cosco in Piraeus, China Merchants in Colombo/Dubai, Hutchison in Hong Kong). This gives them geopolitical significance: e.g. China’s network of port investments along the “Maritime Silk Road” has raised security concerns.

Vertical integration: Shipping lines have leveraged terminals to secure capacity. For instance, MSC (via Terminal Investment Ltd) and CMA CGM (via Terminal Link) operate global terminal networks, ensuring berths for their vessels. Maersk’s APM Terminals is fully integrated with its line. DP World and Hutchison are independent, but their ports serve all carriers. Some commodity traders also own terminals (e.g. Vitol’s stake in the Port of Gibraltar refinery terminal, or Trafigura’s bunkering terminals).

Financials: PSA is not-for-profit but discloses cost-based revenues; DP World (DPW.NYSE) had ~$9.5B revenue and $2B net profit in 2023. COSCO Ports reported ~$4B revenue (2023); China Merchants Port ~$3B. Hutchison Ports is private (under CK Hutchison Holdings). Terminal Link (CMA/China Merchants JV) and CMA itself are private (but CMA CGM reported ~€90B revenue in 2023, some of which is port logistics). The port sector profits are generally stable, and investors are attracted by long-term concessions; DP World’s IPO (2019) reflects global interest.

Trends: Terminal expansion and automation are key trends. PSA’s fully automated Tuas (being phased in 2024–40) is a model. Maersk and Hapag’s “Gemini” shipping alliance has given preference to APMT terminals on certain rotations. DP World has slowed new port projects and is acquiring logistics assets instead. Geopolitical risks (e.g. China’s expanding port footprint, U.S. scrutiny of Chinese-held ports) shape regulatory oversight. Climate and energy shifts are driving LNG terminals and equipment at ports; e.g. Cosco Ports’ new LNG terminal in Qingdao.

Table 2: Major Container Port Operators (2023)

Oil and Commodity Trading Houses

A small group of trading houses dominate global commodity flows – especially in oil and metals. These firms generally operate end-to-end supply chains: buying physical commodities, owning shipping vessels or pipeline capacity, and often running infrastructure. They include:

Vitol Group (private, Switzerland; the world’s largest energy trader). In 2024 Vitol reported ~$331 billion turnover (vs $403B in 2023) and delivered ~7.2 million barrels per day (bpd) of crude and products. It operates ~10,000 retail fuel stations (via Vivo Energy and Petrol Ofisi), ~850,000 bpd of refining capacity (via assets like Italy’s Saras refinery) and has stakes in storage and shipping. Vitol added an ~$8B profit in 2024. It has expanded into power and (recently) metals trading, acquiring firms like Noble Resources. Vitol’s scale and integration (from trading desk to refineries and service stations) give it huge influence over oil markets. It is privately held by founders and management, headquartered in Geneva.

Trafigura (private, Singapore/London). Trafigura’s FY2024 revenue was ~$243.2 billion, with net profit ~$2.76 billion (on ~$243B revenue). It traded ~6.8 million bpd of oil products in 2024 and ~22 million tonnes of metals (copper, aluminum, etc). Trafigura also owns a fleet of about 150 ships (oil and dry bulk). The group has upstream investments (mining interests) and a shipping/logistics division. Vertical integration includes stakes in tankers, warehousing and the recently acquired Greenergy (UK fuels) and refinery interests. Trafigura has faced controversies (e.g. a $1.1B fraud at its Mongolia office), but remains a top global commodities player.

Glencore (public, Switzerland/UK, ticker GLEN). Glencore is a unique hybrid of miner and trader. In 2024 it reported ~$230.9 billion revenue (higher than many oil majors), driven by mining/metals production and marketing, and by its “Glencore Marketing” commodity trading arm. Glencore’s marketing business earned ~$14.4 billion EBITDA in 2024. It mined roughly 1.8M barrels per day of oil-equivalent resources (copper, nickel, zinc etc) and shipped them globally. Glencore is vertically integrated across mining, smelting, shipping, and trading. Its recent acquisition of Viterra (grains) via merger with Bunge highlights its reach. As a publicly listed company (London, Hong Kong), Glencore publishes detailed results and has ~£40B market cap.

Other traders: Mercuria (private, Switzerland) and Gunvor (private, Switzerland) each trade ~$130–150B+ in oil products annually. Both have global offices and owning fleets/tankers. Gunvor has deep ties with Russia (founded by Gennady Timchenko) and trades crude and LNG. BP and Shell (public oil majors) also do large trading volumes but primarily for their own production and refining; they operate global tanker fleets. In agriculture, the “ABCD” traders (private Cargill, ADM, and Bunge and Louis Dreyfus) handle ~60% of grain/oilseed shipments: for example, Cargill (private, USA) is the largest agricultural trader (estimated ~$160B revenue 2023), owning dozens of grain port terminals and major river barge fleets. ADM (public, USA) and Bunge (public, USA) process/ship vast volumes of soy, corn, wheat (each hundreds of millions of tonnes/year) and have revenues on the order of $80–100B. Wilmar (public, Singapore) dominates palm oil and edible oils in Asia. These agribusiness multinationals are vertically integrated: owning farms, crushing plants, shipping, and consumer food brands.

Metals and mining: While Glencore and Trafigura lead in metal trading, major miners like BHP, Rio Tinto, Vale, Anglo American (all public) essentially supply raw commodities (iron ore, copper, coal, etc) to global markets. They have their own shipping (e.g. Vale’s Vale Shipping) and some logistics but are upstream producers, not traders per se. However, they wield market power through production scale (Vale controls ~20% of iron ore trade, for instance).

Trends and geopolitics: Commodity traders benefited from market disruptions in 2021–23 (pandemic shocks, Russia-Ukraine war) to earn record profits; but 2024 saw a normalization (Vitol’s turnover down 18% YoY). Energy transition is a major trend: traders are investing in LNG, biofuels, and renewables trading. For example, Vitol expanded LNG volumes 10% in 2024 and acquired biomass/gas projects. Regulation of trading practices (anti-money-laundering, conflict minerals, sanctions compliance) is tightening globally, affecting these firms. Geopolitically, traders must navigate sanctions (e.g. on Russian oil, Venezuelan oil) and trade war risks (e.g. U.S.–China energy issues).

Logistics and Infrastructure Providers

Beyond shipping and commodities, global trade relies on major logistics integrators and infrastructure firms:

Freight Forwarders and 3PLs: Companies like DHL (Deutsche Post, Germany), Kuehne+Nagel (Switzerland), DB Schenker (Deutsche Bahn), UPS (USA) and FedEx (USA) control large parts of air and land freight networks. DHL operates in 220 countries with ~80,000 vehicles and 250 airplanes (2023 revenue ~$98B). These firms combine air, sea, road and rail networks to deliver cargo door-to-door. Many are publicly traded (DPW, UPS, FedEx, DBK etc.) and report annual revenues of tens of billions. XPO Logistics (USA, partly private) and Panalpina (now part of DSV) are also major players.

Rail and Inland Shipping: Major railroads (e.g. Union Pacific, BNSF in the US; Deutsche Bahn in Europe; Russia’s RZD) and inland barge operators are crucial for continental freight. For example, China State Railway Group moves a significant fraction of China’s exports. These companies (mostly state or semi-state owned) are too many to detail individually but are integral for hinterland connectivity.

Pipelines and Bulk Terminals: Energy and commodity pipelines (e.g. TC Energy for oil/gas, Transneft in Russia) and storage firms (Vopak, Oiltanking) form critical infrastructure. Vopak (public, NL) is the world’s largest independent tank terminal operator (~68 terminals, ~35% market share in independent terminals) handling oil, LNG and chemical products. These infrastructure players often partner with traders/majors to secure flows (e.g. Vitol uses Vopak terminals globally).

Container Leasing: Leasing companies (e.g. Triton International, Textainer, CAI – all public) control ~70% of the world’s 50M+ TEU container fleet. They earn revenue by renting containers to shippers and carriers, indirectly exerting control over equipment supply.

While these logistics firms are slightly outside the scope of “physical trade powerhouses,” they enable trade at each stage. For example, major port operators often form joint ventures with lines (Terminal Link, PSA/Hutchison, etc.) to bundle terminal space with carrier services.

Geopolitical and Regulatory Dynamics

These global companies are enmeshed in geopolitics and regulation:

State Influence: Several key players are state-controlled. China’s influence is evident through state-owned COSCO (shipping and ports) and China Merchants (ports) expanding worldwide, often under the Belt & Road banner. Saudi Aramco (Oil/Gas, state-owned) and Russia’s Rosneft/Gazprom similarly control vast commodity production and trading. Western governments have expressed concern about foreign control of critical ports (e.g. US blocking some Chinese port deals) and critical minerals supply (e.g. cobalt, rare earths).

Regulations and Alliances: New trade rules (e.g. EU’s carbon price for shipping, US CBAM on imports) affect these firms. For example, EU’s FuelEU and ETS extension force shipping lines to reduce emissions or pay. Ports are subject to customs/security regulations (ISO 28000), and commodities are scrutinized (conflict minerals legislation, energy sanctions). Traders and carriers often lobby trade bodies (WTO, ICS) on issues like sanctions and free trade zones.

Market Trends: The drive for supply-chain resilience (after COVID and geopolitical shocks) has led some companies to diversify. For instance, Kuehne+Nagel and Maersk have moved into warehousing and e-fulfillment. Some commodity firms are diversifying into green sectors (Vitol into hydrogen, Trafigura into carbon credits). M&A and consolidation continue: e.g. Glencore+Bunge, CMA CGM’s acquisition of CEVA, and rumors of co-operation between airlines and shipping lines on cargo.

In sum, global trade is powered by a relatively small set of transnational firms. Container shipping is dominated by ~10 carriers; port operations by ~6 major operators; commodities by a handful of traders and producers. These firms’ control of assets (ships, ports, pipelines, storage) and networks gives them significant market power and influence over policy. Understanding global supply chains today means following the moves of these giants as much as counting shipments.